Know the difference between stepped and level premiums

Life insurance premiums are predominantly based on the risk of certain events happening to you. Because health risks increase with age, life insurance premiums will generally increase over time.

That’s why most insurers offer two common ways of paying for, and managing, the costs of your cover over time:

- Stepped premiums: when the cost of your cover is recalculated each year based on your age at your policy anniversary. Generally this means your premium will increase each year as you get older.

- Level premiums: where premiums are calculated based on your age when any cover started. Your premium is generally averaged out over a number of years, which means you avoid increases in your premium due to age at each policy anniversary. This means your cover is more expensive than ‘stepped premiums’ at the beginning of your policy, but generally gets cheaper (relative to stepped premiums) as your policy continues.

Regardless of whether your policy is on stepped or level premium,premium rates and premium factors are not guaranteed or fixed and many life insurers in Australia have repriced premium rates in the past.

Stepped or level premiums – which is right for you?

Generally, this depends on how long you’re planning on keeping your insurance. If you’re planning on keeping your policy for longer than 10-12 years, level premiums may save you money over the life of your policy.

You may also be able to use a combination of stepped and level premiums.

For example, if you think you might want to reduce your level of cover down the track (e.g. when you're kids are grown up or you've paid down debt),you may be able to use level premiums for the portion of cover you think you'll keep longer and stepped premiums for the additional cover.

This is something your financial adviser can help you with.

Repricing is a possibility regardless of which structure you choose

It’s important to note that at policy anniversary the premium may still increase (even with level premiums), because age is just one factor that determines your premium. Other factors that impact premium (such as claims trends in Australian population) can result in a repricing of your insurance cover.

When insurers reprice stepped or level premiums, they don’t do it for an individual policy within a specific group unless they do it for every policy in that group.

To decide whether you’re better off on stepped or level premiums going forward, we recommend you speak to your financial adviser. They can help you understand your policy as well as any repricing activity that’s recently occurred, so you can make an informed decision.

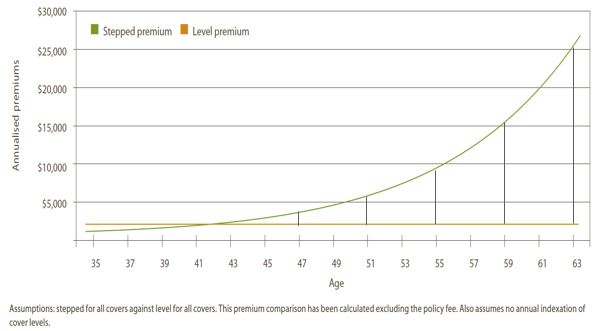

A graphical example

Below is an illustration of stepped v level premiums, showing the difference between the two when you look at increases due to age. Other types of premium increases aren’t shown on this graph.

For illustrative purposes only. This graph illustrates age-based premium increases for stepped against level for all covers. This premium comparison has been calculated, assuming all other factors affecting the premiums are excluded.

Both stepped and level premiums can increase due to factors other than age.

Premium rates and premium factors are not guaranteed or fixed, and insurers have increased premium rates in the past and may increase in the future.

We recommend that you refer to the relevant product disclosure statement and policy documentation, and speak to your financial adviser, to understand other factors affecting your premiums.

To decide whether you’re better off on stepped or level premiums going forward, we recommend you speak to your financial adviser.