Life cover 101

It may be the simplest form of life insurance, but life cover is undoubtedly one of the most important as it helps you provide for your debts and dependants. When you’re looking at life cover, there are 3 key things you need to understand so you know what you’re covered for, and what that means at claim time:

- How much you’re covered for

- How your policy will be paid out

- How your cover is structured – linked or stand-alone.

1. How much are you covered for

It might sound obvious, but you need to think about the reasons you takeout life cover when you apply for cover.

You might think “$1 million should be enough” – but have you thought about how much money would really be needed to replace your income, support your family, educate your children etc.?

The Australian Securities and Investments Commission (ASIC) has developed a Life insurance calculator that can help. But the best way to find out how much cover you need is to talk to a financial adviser.

Just as importantly, an adviser can help you adjust this figure over time as your debts reduce or your children become less financially dependent. That way you’re not paying for cover you no longer need.

Income replacement calculator

Income replacement calculator

Instructions

- Enter your current income (before tax and including superannuation contributions) into the green text field or click and drag the green circle underneath it to set it.

- Your projected income over the next 30 years will appear in the graph.

* Assumes a salary increase of 2% per annum and continuous income

2. How your policy will be paid out

When a life cover benefit is paid, it’s generally paid to the owner of the policy or a nominated beneficiary. In many cases the policy owner will be your spouse or your estate.

But what if your policy is owned inside super?

In this case, the policy owner is the trustee of the super fund – meaning they receive your benefit from the insurer. The trustee will then pay your benefit to the beneficiary(s) you’ve nominated, or your estate.

What you need to know about life cover inside in super is that there are different rules around how benefits can be paid, and how they are taxed, so it’s best to seek financial and tax advice specific to your situation. The same can be said for business owners, as there are specific life cover strategies you can use to protect yourself or your business.

You may also want to consider the best way to support your beneficiaries. For example, you may want your life cover benefit to be paid partly as a lump sum and partly as ongoing payments – which could help your loved ones take care of immediate expenses (e.g. pay down debt) and ongoing living costs.

Did you know? There’s a common exclusion on life cover policies that means you’re generally not covered for suicide for first 13 months of taking out cover or reinstating your policy. You can find details of any exclusions in the relevant Product Disclosure Statement (PDS).

3. How your policy is structured – linked or stand-alone

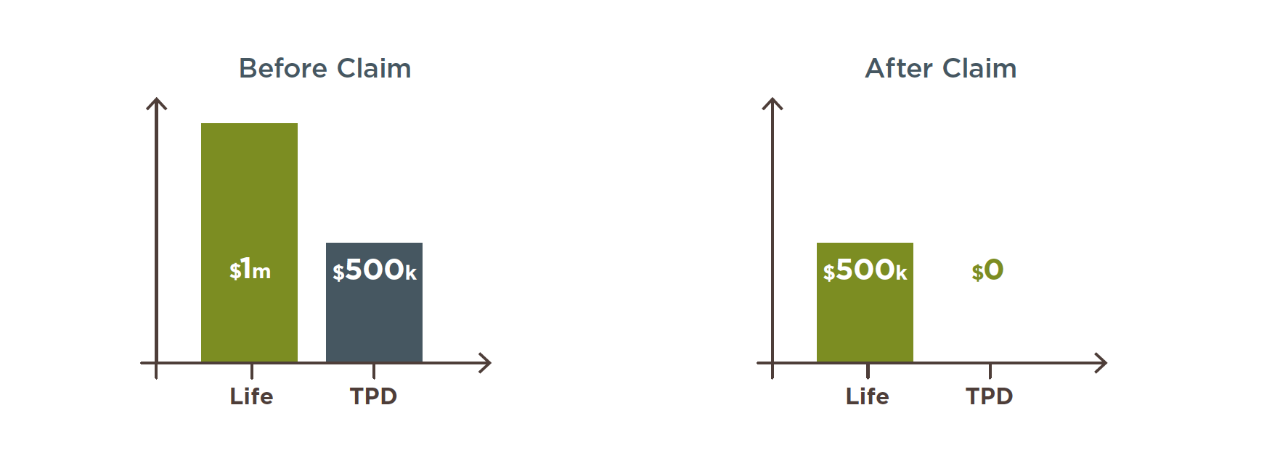

Life cover may be purchased as a stand-alone policy or as a ‘linked policy’ that’s connected to TPD cover or trauma cover. Linking policies generally reduces your premium, but there are implications at claim time.

Say you have a $1 million life cover policy linked to a $500,000 TPD cover policy. If you make a successful claim on your TPD cover, your life cover benefit will reduce by the $500,000 paid out.

Depending on your situation you may be eligible to buy back this extra life cover at some point, but it’s important to note that your life cover is significantly reduced in the meantime.

OneCare is issued by Zurich Australia Limited (Zurich) trading as OnePath Life (OneCare) ABN 92 000 010 195, AFSL 232510. OneCare Super is issued by OnePath Custodians Pty Limited (OnePath Custodians) ABN 12 008 508 496, AFSL 238346. Zurich and OnePath Custodians are not related bodies corporate.

We recommend that you read the relevant Product Disclosure Statement available at www.onepath.com.au or by calling 133 667 before deciding whether to acquire, or to continue to hold the product.

It is current as at July 2023 but may be subject to change. Updated information will be available by contacting Customer Service on 133 667.

Whilst care has been taken in preparing this material, Zurich Australia Limited and its related entities do not warrant or represent that the information is accurate or complete. To the extent permitted by law, Zurich Australia Limited and its related entities do not accept responsibility or liability from the use of the information.

Where tax or technical information is needed, the information is our interpretation of the law and does not represent tax advice.