When you apply for income protection, you can generally choose a sum insured that’s up to 70% of your before-tax income (excluding super contributions).

Income protection 101

There's not much you can do without an income. In monetary terms, your ability to earn an income is your biggest asset by far - which is why income protection is so important. When you’re protecting your biggest asset, there are 3 things you need to understand so you know what you’re covered for, and what that means at claim time:

- How much you’re covered for – the sum insured

- How long you need to wait to be eligible to make a claim – the waiting period

- How long your claim will be paid for – the benefit period.

1. Sum insured

The higher your amount insured, the higher your premium will be. So you need to think about how much money you’ll really need to keep up with your everyday expenses (like your rent/mortgage, bills, school fees etc.). Just because you can cover 70% of your income doesn’t mean you have to.

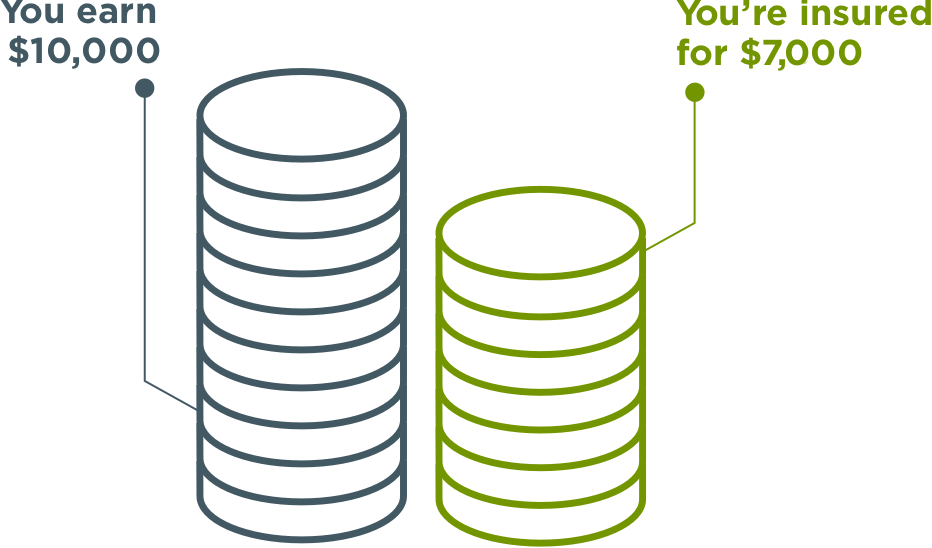

For example, you might earn $10,000 per month but decide you only need $5,000 per month to keep up with your living costs. That may significantly reduce the cost of your cover (i.e. your premium).

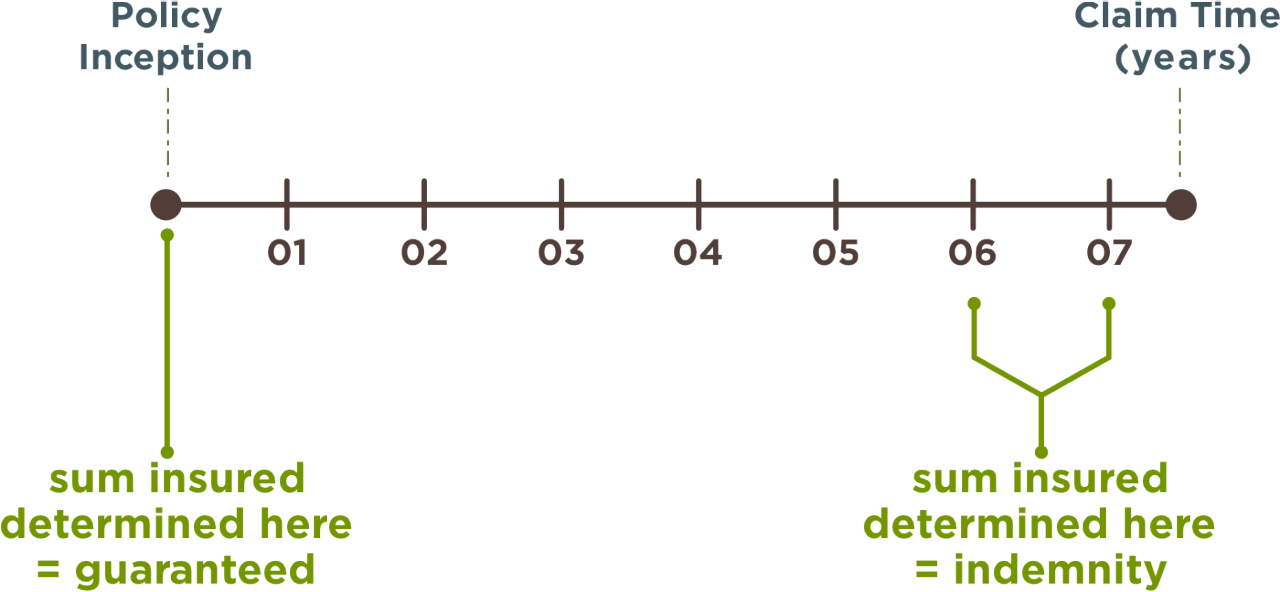

You can also reduce your premium by choosing an ‘Indemnity’ benefit payment type.

This means the amount you receive will be determined by your actual income in the two years before the claim (which could mean you receive less than the amount insured) – as opposed to a ‘Guaranteed’ or ‘Agreed’ payment type where, at claim time your amount insured won’t be adjusted if your income has decreased.

Note: 'Agreed value' income protection policies guarantee the amount you'll be paid if you have to make a claim – regardless of any changes to your earnings. However, from the 1 April 2020, this type of policy is no longer available with OnePath.

Use the income replacement calculator to forecast your current income into the future, to help you decide on a amount insured.

2. Waiting period

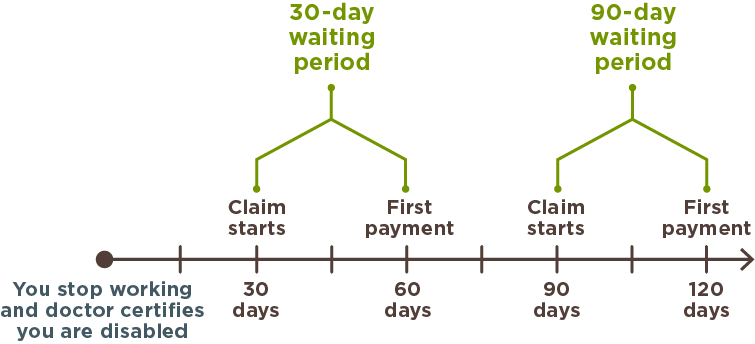

The waiting period is the number of days before you become eligible to claim,starting from the date the doctor confirms you are disabled. The most common chosen waiting period options are 30 days, 60 days and 90 days.

Income protection payments are usually made monthly in arrears.So if you had a 30-day waiting period, your first payment would be made 60 days after you first became disabled.

The waiting period affects the premium. Naturally, a policy with a 30-day waiting period is more expensive than the same policy with a 90-day waiting period, because you’re eligible to claim sooner.

For example, if you’re off work for 80 days and have a 30-day waiting period, you could potentially be paid your amount insured for 50 days. But if you have a 90-day waiting period, you may not be eligible to receive anything.

When choosing your waiting period, you should think about how soon you’re likely to need financial support if your income stops:

- If you have access to sick leave or annual leave, or a high level of savings, you may be able to take a longer waiting period and reduce your premium.

- If you’re a casual employee or business owner, or you have a low level of savings, you may want a shorter waiting period, bearing in mind your premium will be higher.

3. Benefit period

The benefit period is the maximum amount of time you can receive income protection payments for any claim while you are disabled. It can be based on time (e.g. 2 years) or age (e.g. to age 65) and your choice can make a difference to the total amount you receive.

Say you’re aged 40 and you become permanently disabled, meaning you’ll never be able to return to work. If you had a 2-year benefit period, your benefit payments would stop when you’re aged 42. But if your benefit period period was to age 65, you would continue to receive benefit payments for an additional 23 years as you continue to meet the disability definition.

Choosing a longer benefit period increases your premium because the potential payout is higher. However, be aware the benefit period is the maximum amount of time you can receive payments. If you’re able to return to work sooner than that, or you reach age 65, your payments will stop.

Also, if your policy offers ‘partial disability benefits’, you may be able to return to work part-time and receive reduced payments until you’re able to work to full capacity. This can be a great benefit to have as it means you're supported if you're restricted in your capabilities, or you want to try a new occupation.

Oh, and one more thing…

One great feature of income protection (outside superannuation) is that premiums are generally tax-deductible, which can make it significantly more cost-effective to get the cover you need.

You may also be able to hold an income protection policy inside super, meaning you can use tax-effective super contributions to pay your premiums, however, within a superannuation policy, features are generally more restricted.

If receiving payment for an income protection claim (outside super) OnePath does not withhold tax (under the PAYG withholding system) from claim payments, so it is advisable that you retain your payment statement for your tax records and include the claim payments received in your tax return (however you should seek tax advice to understand your personal tax liability).

Check your cover now

If you have OneCare Income Secure Cover, you can see exactly what you’re covered for by logging into the Self Service Portal. There you can update your details and change your communication preferences.

In particular, check your cover against our income replacement calculator. If your income has changed significantly since you last updated your policy, there’s a chance you may be over or under-insured – in which case you should talk to your financial adviser.

Did you know?

There’s a common exclusion on income protection policies that means you generally won’t be covered if you suffer an injury or illness because of an intentional act. Also,if your cover is held inside super, you’re generally not covered if you suffer an injury or illness while you’re unemployed.

OneCare is issued by OnePath Life Limited (OnePath Life) ABN 33 009 657 176, AFSL 238341. OneCare Super is issued by OnePath Custodians Pty Limited ABN 12 048 508 496, AFSL 238246. OnePath Life is not a related body corporate of OnePath Custodians.

We recommend that you read the relevant Product Disclosure Statement available at www.onepath.com.au or by calling 133 667 before deciding whether to acquire, or to continue to hold the product.

OnePath Life Limited (OnePath Life) ABN 33 009 657 176, AFSL 238341. It is current as at September 2019 but may be subject to change. Updated information will be available by contacting Customer Service on 133 667.

Whilst care has been taken in preparing this material, OnePath Life and it's related entities do not warrant or represent that the information is accurate or complete. To the extent permitted by law, OnePath Life and it's related entities do not accept responsibility or liability from the use of the information.

Where tax or technical information is needed, the information is our interpretation of the law and does not represent tax advice.